The vast amounts of capital now being deployed across ESG assets has, in recent years, led to financial innovation in the form of ESG-related equity derivatives. In a new paper, GAM Systematic’s trading team, Shamir Pandya, Wanpin Zhuang and Joe Devine, map the evolutionary journey from launch to present of the three most liquid ESG index futures and assess their current tradability from a systematic perspective.

30 May 2022

Click here to view the GAM Systematic white paper in full.

Sustainability as an investment consideration began in Europe, but we are now seeing heightened interest in environmental, social and governance (ESG) investing across all regions, none more so than from equity market investors. According to Morningstar, equity portfolios currently account for 55% of all ESG assets under management. With vast amounts of capital being deployed, this naturally creates financial innovation in the form of ESG-related equity derivatives that we believe may help assist market participants with their various investment and risk management needs.

ESG equity index derivatives – essentially tradable indices that adjust holdings based on ESG considerations – are in their nascent phase of trading activity, especially if one compares them to their underlying and more liquid benchmark equity indices. However, we see substantial and growing interest in this type of exposure from a wide array of market participants.

Part of our daily trading desk activities includes engagement with the relevant exchanges and counterparties. In our conversations with EUREX, CME and OMX – home to the most liquid ESG index contracts – they each explained that the path to introduce ESG equity derivative products was initially driven by long only equity mandates. However, as the ESG space has garnered much more interest, particularly in the period since the Covid outbreak, a more diverse set of market participants are expressing interest and steadily dipping their toes in to trade ESG index futures.

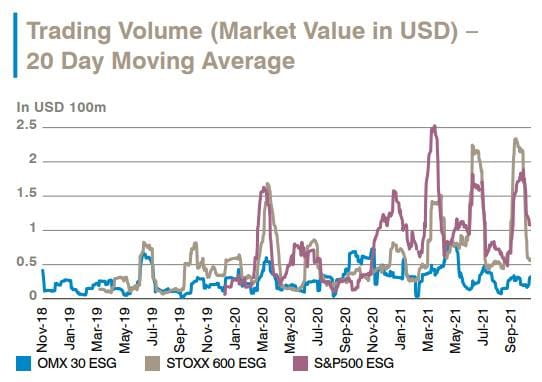

In our latest paper, we look at the three most liquid ESG index futures (the E-mini S&P 500 ESG index, STOXX Europe 600 ESG-X index and OMX Stockholm 30 ESG Responsible index contracts), which together make up more than 90% of global ESG index trading volume, with the aim of assessing the current tradability of ESG linked equity contracts.

Source: GAM, Bloomberg. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered a recommendation to buy or sell securities or investment advice.

We map the evolutionary journey from launch to present of each of the index futures, look at growth in daily volumes and open interest, as well as the current liquidity landscape. Data analysis of order book liquidity and bid/offer spreads provides an insight into the implied trading costs of each contract, upon which we draw the conclusion that ESG futures can now offer enough liquidity to trade at a reasonable cost.

GAM is an independent, global provider of asset management services operating in three principal fields: investment management, wealth management and third-party fund management services. Across all areas of our business we are committed to the pursuit of highly differentiated strategies, having long recognised that results beyond the ordinary are best achieved by thinking beyond the obvious.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. There is no guarantee that forecasts will be achieved. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Assets and allocations are subject to change. Past performance is no indicator for the current or future development.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. There is no guarantee that forecasts will be achieved. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Assets and allocations are subject to change. Past performance is no indicator for the current or future development.