Amid ongoing investor fervour for artificial intelligence (AI) stocks, Wendy Chen discusses her key takeaways from the COMPUTEX Taipei IT trade show, and shares her take on how the latest tech developments square with elevated valuations across the sector.

08 July 2024

For all the talk of a potential tech bubble, it feels like investors just cannot get enough of tech stocks, especially those sprinkled with AI stardust. To put this in some context, as June’s COMPUTEX extravaganza convened, the tech-focused NASDAQ Index was around 20% higher year-to-date, and an amazing 40% above the lows of October last year. Over the same periods, AI pin-up Nvidia was up by 143% and 191% respectively, briefly overtaking Microsoft to become the world’s most valuable listed company.

While all the major industry players, like Intel, AMD, Qualcomm and Nvidia had their CEOs present at COMPUTEX to meet suppliers, customers and investors, it was the latter that attracted the lion’s share of the attention. And if any company has come close to living up to all the AI-related hype lately, then Nvidia is surely the one, building on its market leadership in the graphics processing unit (GPU) market with increased dominance in dedicated AI chips, especially those designed specifically for datacentres and systems driving corporate AI chatbots, and reigning supreme in crucial AI-training chipsets.

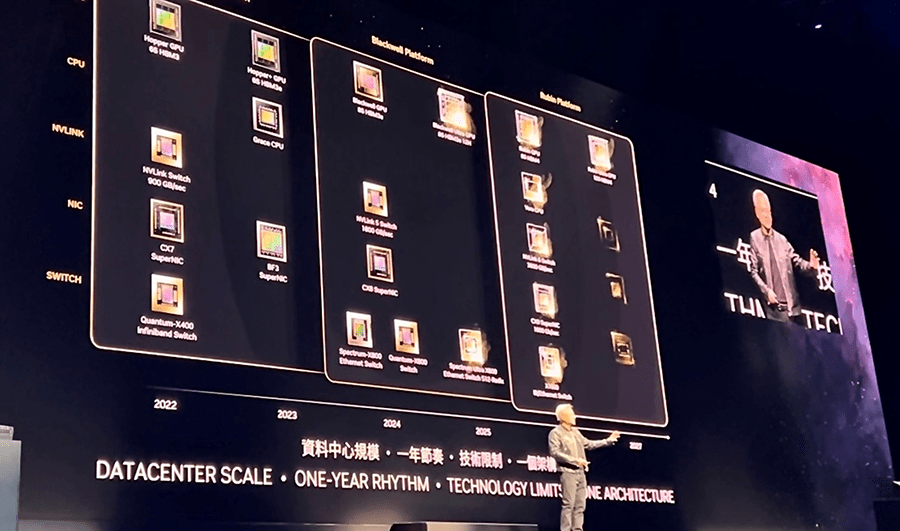

Never content to rest on his laurels, biker jacket-clad Nvidia founder and CEO Jensen Huang – memorably called the “Taylor Swift of tech” by none other than Mark Zuckerberg – set out an ambitious roadmap for the firm’s development, starting with news of faster-than-expected product cycles. For example, not only will the GPU platform see a new product generation every year, Nvidia will deliver a whole new platform every two years. So we can expect the Blackwell GPU platform to roll out in 2024 and into 2025 with the new Ultra chip, followed by the new ‘next-gen’ AI Rubin and Rubin Ultra platform now teased for 2026/27, promising both cost and energy savings.

Nvidia: defying gravity and Moore’s law

Jensen Huang took centre stage with roadmap of Nvidia products all the way to 2027

Source: GAM

Breaking Moore’s Law of chip innovation?

Way back in 1965, Intel co-founder Gordon Moore famously observed that the number of transistors in new integrated circuits can realistically double every two years at minimal cost, driven by greater production expertise. Although the pace of semiconductor advancements had been slowing since 2010, Nvidia appears to have upended recent trends, with a 30x advancement in computing power in a decade. What this means is that, even setting aside projected future product advancements, using the current Blackwell GPU to train ChatGPT 4 requires only about 10% of the GPU needed just two years ago on its Hopper architecture.

Memory in the AI era: Don’t You (Forget about Me)

While AI trailblazer Nvidia has understandably attracted much of investors’ attention, both at the Taipei event and beyond, in our view it is important to look for investment opportunities beyond the increasingly crowded GPU space. If power is nothing without control, then AI chipset power is nothing without memory; in fact, AI servers generate immense volumes of data, so require vast banks of compound or high-density flash memory to perform. So next-generation AI GPUs in servers and accelerators produced by Nvidia (and others) look set to drive demand for memory produced by companies like Micron and SK Hynix. Memory producers were already benefitting from the ending of the two-year oversupply situation and the AI/GPU boom is driving the upturn in their outlook. By way of example, every Nvidia GB200 GPU shipped requires about eight High Bandwidth Memory (HBM) chips – an emerging kind of vertically stacked memory featuring low power consumption and ultra-wide communication lanes. So Nvidia and HBM manufacturers have formed a very timely and potentially lucrative collaboration, highlighting how the AI boom is bolstering revenues across other players in the memory sector, including Micron and SK Hynix.

Closing the laptop lid on hopes that AI can boost the PC replacement cycle

With the PC market still largely wallowing in a three-year downturn of its own, it is understandable that the likes of Acer, Asus and Lenovo are keen to hitch a ride on the AI bandwagon. And while some investors have been getting excited about the prospects of an AI capability-induced upturn in the PC replacement cycle, we are far from convinced. Even with 20 or so new AI PCs launched at the three-day COMPUTEX event, we see limited differentiation between brands, pretty much all of which run on the same Qualcomm Snapdragon Elite processor, enable the same Microsoft Copilot, and are largely mass produced across the same outsourced production lines in Taiwan. While the AI PCs’ capabilities are still developing, for the time being at least, they cannot replace the capacity of a fully functional AI server. We are not convinced that the benefits in day-to-day usage of ‘edge computing’ – doing the AI computing on your end device, like smartphones and PCs, rather than on the cloud with, for example, Copilot – represent any real improvement that most users of Excel, Word etc would be prepared to pay much extra for.

Why the cooling system sector looks overheated

As noted by Jensen Huang and many others, with the AI boom demanding increasingly powerful GPUs and ever-greater memory requirements, tech sector demand for energy management, and especially cooling systems, is rising. Some stocks most associated with liquid cooling, like AVC and Auras Technology, have seen their stock prices more than double year-to-date on such sentiment hype. However, we take the view that the exuberance is misplaced, as the barriers to entry in this market don't seem that high and competitors/aggregators are already working on their own solutions. In short, so many players could quickly enter the cooling market and existing suppliers appear to have little by way of any sustainable competitive advantage.

Apple’s AI approach – not core, for now

While Apple did not participate in the Taipei event, its own annual Worldwide Developers Conference (WWDC) attracted much interest during the month. Despite its considerable clout in the consumer devices market and showcase of Apple Intelligence (with a more sensible Siri, finally), Apple has maintained a fairly conservative stance to edge AI innovation, seemingly favouring cloud-based, with edge computing on the upcoming iPhone a slim prospect. But, such is its foothold in the mobile devices market, we think Apple has the capability to become a much bigger story in AI, and particularly the edge computing space, with real potential to steal some of the limelight from OpenAI and Nvidia over the years ahead.

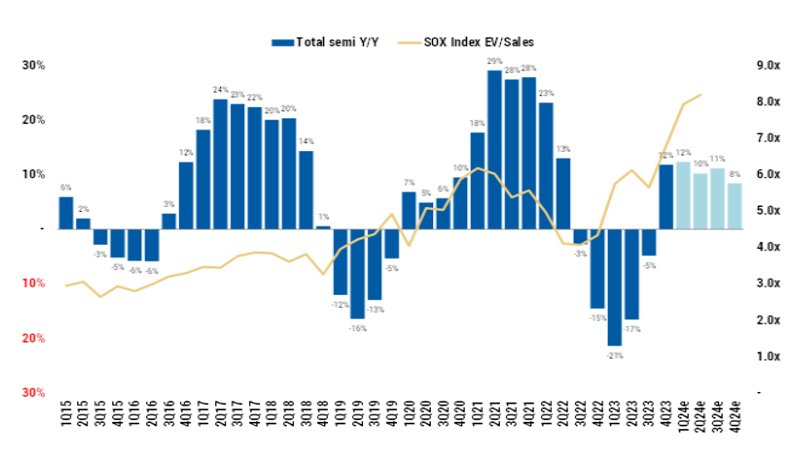

Semi infra capex build-up not yet concluded

Valuations near prior peaks, as fundamental recovery starts

Source: Company data, SIA, Morgan Stanley Research

Outlook: ‘picks & shovels’ winners are still taking it all

Overall, despite the frenetic pace of development, in our view the AI market remains largely in the infrastructure stage, hence the market’s focus on the most innovative of hardware developers, Nvidia. We see scope for further growth in the infrastructure sector; with the capex build-up having further to run, we are seeing interesting opportunities across the supply chain, including on the foundry side (such as TSMC) as well as memory suppliers (such as Micron and Hynix). All the while, the application sector has continued to broadly lag. In time, we expect the applications side to attract more attention, as end user clients put the infrastructure to work in generating revenues, becoming a profit driver rather than a cost. But for now, while hyperscalers like Google, AWS and Meta have been upping their capex to build their AI infrastructure, such is the pace of hardware development, concerns persist that some of the hardware could soon begin to feel outdated, possibly in a matter of two or three years. So, for us, the focus remains on the infrastructure developers and their supply chains, all the while being vigilant to opportunities on the applications side ahead of an eventual healthy rebalancing of the AI market.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.