Impressive results from Europe’s banks continue to reflect years of balance sheet strengthening, regulatory changes and the end of the era of rock-bottom interest rates.

27 February 2024

While commercial property exposure remains a worry for some US banks, exposure to falling asset values is very limited on this side of the Atlantic, and highly concentrated in a few specialist institutions. Atlanticomnium’s Romain Miginiac argues that with Europe’s banking sector in rude health, any talk of contagion is greatly exaggerated.

Against a backdrop of growing concerns about commercial real estate (CRE) exposure in certain parts of the financial sector, European banks’ fourth-quarter earnings remained rock solid. From a bondholders’ perspective, another quarter of double-digit return on equity (RoE), near-record capitalisation and resilient asset quality ticked all the right boxes.

Despite the increased focus on potential headwinds, in our view, these are manageable through earnings alone and will not derail the sector’s robust credit story.

Focus on banks’ earnings buffer, not earnings momentum

Over the last few weeks, European banks have again delivered solid results, with earnings in line with consensus expectations. 2023 was a stellar year for banks, with the sector finally delivering double-digit RoE - around 12% in the 2023 financial year (FY).

Over the last few quarters, the market began to focus on “peak earnings” as the impact of higher interest rates fed through to banks’ top and bottom lines. Talk of rate cuts starting later in 2024, combined with other headwinds – such as deposit repricing, cost inflation or higher loan loss provisions – will likely offset some of the prior uplift.

Nevertheless, the European banking sector is still expected to deliver healthy profits over the coming years – with 10-12% RoE consensus expectations over the full-year FY24-25, compared to approximately 5% over FY18-22.

European banks expected to make double-digit returns in FY24 and FY25

Source: Atlanticomnium, Bloomberg, as of 12 February 2024

From a bondholders’ perspective, earnings momentum is marginal for European banks’ credit profiles. The focus should remain on banks’ earnings buffer – the ability to absorb credit and other losses (such as market risk and litigation). With solid double-digit RoE expected over the coming years, European banks can absorb sizeable levels of losses before excess capital is eroded.

To put the sheer amount of extra revenue these banks are producing into perspective, according to European Banking Authority data, EU banks generated an annualised EUR 180 billion in net income per quarter as of Q3 2023, compared to around EUR 90 billion on average over the past five years (Source: European Banking Authority, Q3 2023 Risk Dashboard).

Capital metrics near record-high levels

Q4 did not show a major shift in European banks’ capital metrics. Common Equity Tier 1 (CET1) ratios, which demonstrate a bank’s capital buffers, remain near record-high levels. On average, large European banks have CET1 capital ratios around 15%, representing more than 400 basis points (bps) of excess capital to regulatory requirements. Large buffers of excess capital form another sizeable layer of protection for bondholders against loan losses, on top of earnings’ buffers.

As an example, BBVA had a buffer of excess capital of around 390 bps over requirements, or EUR 14.2 billion in absolute terms. On top of that the bank generated EUR 17.9 billion of pre-provision profits – meaning that in any given year the bank would need to take losses of more than EUR 30 billion to deplete both its earnings and excess capital buffers – that is equivalent to roughly 8% of loans. At the peak of the Eurozone crisis, the bank took credit losses equivalent to slightly over 2% of loans – hence it would take losses roughly four times higher than during the worst year of the 2007-08 Global Financial Crisis (GFC) and the subsequent Eurozone crisis to wipe out earnings and capital buffers. Earnings alone would cover more than twice this level of losses.

Looking ahead, capital levels are expected to remain strong – albeit decline modestly from record-high levels, as several European banks operate with capital ratios above management targets. It is unlikely that the sector will experience any material depletion of capital buffers, driven by both a tight regulatory environment and ongoing macro uncertainty.

With the implementation of Basel IV still on the horizon, and EU banks’ capital requirements having increased in recent quarters – regulation remains a key positive catalyst for bondholders – the effect has been to force capital preservation. Regulators remain highly proactive in managing banks’ capital requirements, through both macro and micro prudential measures such as higher countercyclical buffers or bank-specific add-ons for particular pockets of risk.

Asset quality remains stubbornly resilient

European banks have consistently demonstrated the quality of their lending books, as non-performing loan (NPL) ratios remain persistently low and provisions for loan losses mostly came out below expectations in Q4. Despite high macro uncertainty and pockets of vulnerability in certain sectors, exposures remain resilient.

The most topical area of European banks’ lending books is CRE – following drastic price action in the equity and bonds of certain players in the US, Japan and Germany. CRE tends to be a periodic area of concern, not least of late, with property prices, particularly offices, under significant pressure. However, the handful of banks highly concentrated in CRE is fairly unique – as highly concentrated on CRE, for example PBB in Germany being a monoline CRE lender with exposure to the US.

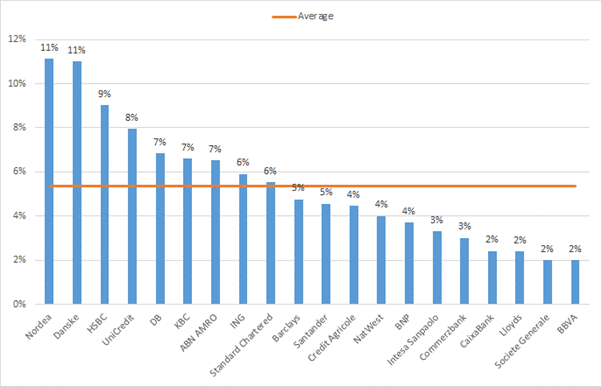

Nobel Prize laureate Harry Markowitz famously said that for investors, diversification is the only free lunch. This is particularly true when assessing the potential impact of banks’ CRE exposures. Large European banks have a relatively modest exposure to the sector (roughly 5-10%). This limits the impact should credit losses start materialising – a mere earnings headwind, even in the worst case. Therefore, potential vulnerabilities for a small number of [European] banks due to outsized CRE exposures typically have no wider sector impact.

The 20 largest listed European banks (Stoxx 600 banks) by total assets have circa 5% exposure to CRE

Source: Atlanticomnium, company reports as of last filing date

Moreover, when assessing the potential impact of such exposures, quality is as important as quantum. The bulk of these are secured, with low average loan-to-value ratios (around 50%), well-diversified by geography and property type. The US (in particular, office space) only forms a marginal part of European banks’ exposures.

Overall, Q4 earnings have been supportive for bondholders, given strong earnings buffers, large excess capital buffers and resilient asset quality. Large European banks can absorb a more stressed scenario through earnings alone, and CRE is a modest headwind for earnings, rather than a credit story.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.